Smarter Screening, Stronger Occupancy: How Cash Flow Data Surfaces Qualified Renters

Your screening process is designed to keep bad residents out. The question is whether it's also filtering out good ones.

Most property managers screen on credit. Credit scores can give you a useful signal on delinquency risk, but roughly 44% of renters have credit scores below standard acceptance thresholds, and that share grows further when accounting for the 10% of Americans with no credit record at all.* That means a credit-based screening process excludes a significant portion of renters in your leasing funnel.

Credit scores reflect how someone has managed debt in the past, but not necessarily whether they can pay rent reliably today. Inside your declined and conditionally-approved applicant pool, there are qualified renters with strong cash balances, consistent inflows, and spending discipline. Cash flow data can help find them.

When you layer bank transaction data into the screening process, a meaningful subset of qualified renters emerges from within the no or low score group. Applicants who are below the credit acceptance threshold but have strong cash flow carry higher bank balances, more expense coverage, and rarely let their balance drop near zero compared to others in their credit band. Some even outperform prime applicants who would pass a standard credit check outright.

26-37% of declined and conditional applicants have the cash flow of a qualified renter and can be safely approved within your risk profile.

Cash flow data surfaces those applicants so you can approve more qualified renters without taking on more risk. Properties already using cash flow screening are capturing this leasing volume. This report shows how to do the same before those applicants sign elsewhere.

*https://www.federalreserve.gov/econres/notes/feds-notes/measuring-renters-in-credit-data-evidence-from-linked-survey-and-administrative-data-20260508.html

What Credit Scores Miss

Credit scores are a standard part of the leasing process for good reason. Better scores correlate with better payment outcomes, as eviction rates in the worst score bands run 40 times higher than those in the best.

Credit scores lose predictive value when the population you are screening has weaker credit profiles to begin with. Renters have lower credit scores and higher delinquency rates than the broader consumer population on average, and skew toward younger adults and lower-income consumers who are also more likely to have thin or no credit files.* Roughly 44% have scores below 660, and that share grows when accounting for the approximately 10% of Americans with no credit record at all.*

That means a large portion of the applicant pool either falls below standard thresholds or cannot be scored at all, putting more pressure on the screening process to fill the gaps. Automatic declines cut off applicants who may well be able to pay, while conditional approvals with requirements such as co-signers, larger deposits, or shorter initial lease terms add friction to the process, create additional administrative burden, and risk losing the applicant altogether before a lease is signed.

The deeper issue is that credit scores were designed to measure debt repayment, not what property managers actually need to know: can this applicant reliably cover rent each month. Cash flow data answers that directly.

*https://newsroom.transunion.com/transunion-analysis-collection-records-are-highly-predictive-of-resident-behavior/ https://files.consumerfinance.gov/f/201505_cfpb_data-point-credit-invisibles.pdf

What Cash Flow Data Shows

Cash flow analytics look at an applicant's actual banking activity, including income, cash balance, and spending patterns, to assess their current financial position rather than just their credit score.

We analyzed cash flow data from rental applicants below common credit score thresholds, looking at three key metrics:

Median cash balance: the typical amount an applicant keeps in their account month to month, reflecting whether they maintain a financial cushion or are often stretched thin

Expense cushion: how many days of expenses their cash balance could cover in a given month without any new income coming in, a measure of financial resilience.

Days below $100: how often their balance drops below $100 in a given month. A balance that low leaves little room to cover rent when it's due and is a predictor of falling behind.*

Within these applicants, we surfaced those with strong cash flow, defined as having a NovaScore Cash Flow (NSCF) of 650 or above. NSCF is a predictive cash flow score derived from bank transaction data, analyzing income consistency, cash reserves, and spending patterns to assess an applicant's current financial health.

*https://www.consumerfinance.gov/data-research/research-reports/behind-on-rent-examining-rental-housing-delinquencies-in-new-payment-data/

The No Score and Thin File Opportunity

With little to no credit history on record, no score and thin file applicants give a credit-based process almost nothing to evaluate, pushing them toward a conditional approval or decline by default. Cash flow data fills that gap.

As a group, these applicants carry a median cash balance of $1,282 and about 7 days of expense coverage, spending around 7 days per month with less than $100 in their accounts. That profile explains why credit-based screening flags them. There is limited buffer if expenses spike or income is delayed.

Within that group, applicants with strong cash flow scores look meaningfully different. Their median balance is $4,886 and they maintain approximately 25 days of expense coverage, meaning their cash balance alone could cover a full month of expenses before income needs to kick in. They drop below $100 only 1 day per month. That kind of financial cushion suggests a renter who can handle the recurring obligation of rent without difficulty.

The Near-Prime Opportunity

Near-prime applicants, those with credit scores between 600 and 660, fall into the conditional approval range for many Class A and B properties.

As a group, near-prime applicants carry a median cash balance of $934 and about 5 days of expense coverage, spending around 8 days per month with less than $100 in their accounts. The limited buffer makes a missed or late rent payment a real possibility.

Within that group, applicants with strong cash flow scores have a meaningfully different profile. Their median balance is $3,322, almost 4 times the broader near-prime group, and they maintain roughly 13 days of expense coverage. They only spend 2 days a month with a balance below $100, a pattern that reflects consistent financial management.

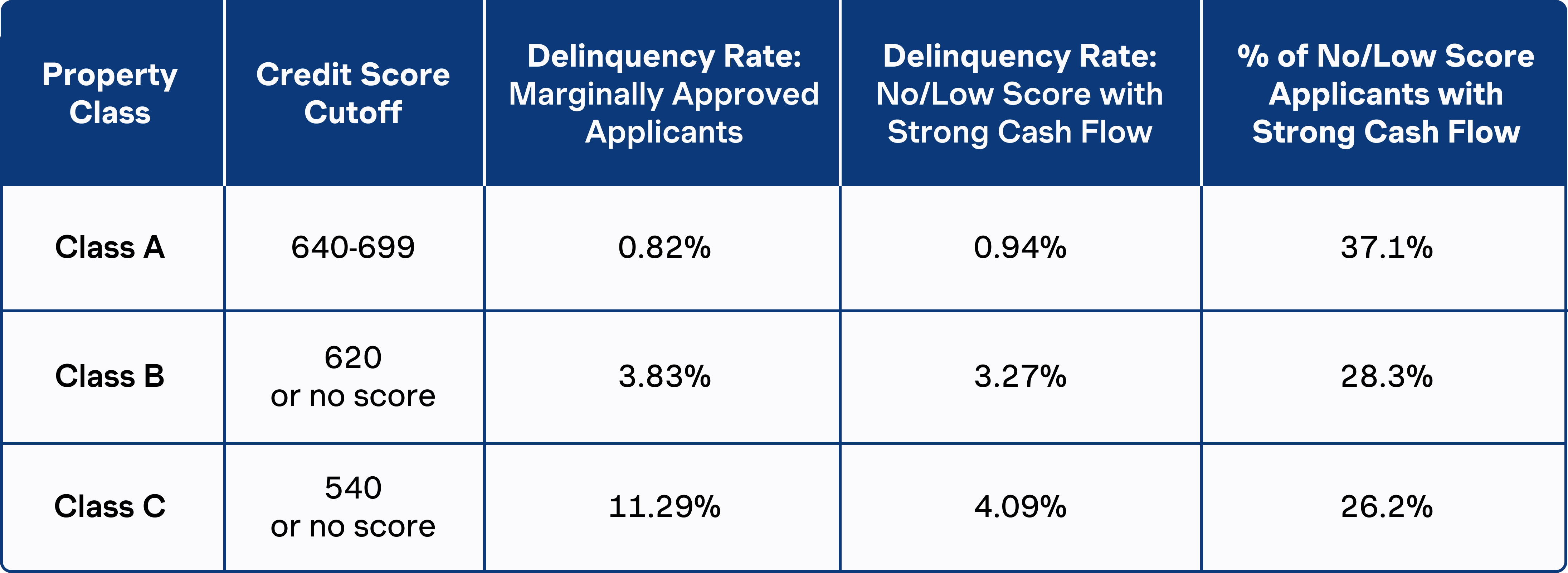

How Cash Flow Can Predict Delinquency

To understand whether cash flow data could support expanding approvals without increasing delinquency risk, we compared outcomes* between marginally approved applicants (those in the lowest approved credit score band) and those with low or no credit scores but strong cash flow. We ran this analysis across Class A, B, and C properties using proxy credit score thresholds intended to reflect common industry cutoffs.

Low and no score applicants with an NSCF of 650 or above show delinquency rates comparable to or better than the applicants you're already approving at every credit threshold. For Class B and C operators, this translates directly to a better delinquency profile alongside higher approvals, and even at Class A the leasing volume comes without a meaningful increase in risk.

Across all property classes, the data points to the same conclusion: cash flow screening creates an opportunity to expand approvals while maintaining a risk profile that aligns with your portfolio objectives.

*Delinquency is measured as 90 or more days past due on an auto loan within a 12-month window. This threshold also closely mirrors observed delinquency rates in rental housing, reinforcing its use as a proxy for rent payment risk.

26-37% of applicants in your declined and conditional pool could be safely approved, representing real leasing volume already in your pipeline.

The Cost of a Missed Approval

Every strong-cash-flow applicant you decline or only conditionally approve is a missed approval that carries a real, measurable cost.

At a national average rent of $1,750 per month, a vacant unit costs roughly $58 per day in lost revenue.* For every vacancy, about 9 renters apply for the unit,* and roughly 5 of them fall below common credit thresholds. Of those 5, our analysis shows 1 to 2 actually have the cash flow to pay rent reliably. Standard credit screening declines them anyway.

For a 100-unit building turning over 46 units per year, that means roughly 58 qualified applicants are declined annually — not because they can't pay, but because their credit score doesn't reflect it.* Each missed approval equals missed revenue in the form of 1 to 2 weeks of vacancy, totaling $34,000 annually.* Property managers can capture this missed income and increase overall property NOI through cash flow screening on the same tenant base.

Screening delays from missed applicants cost a 100-unit building roughly $34,000 annually, a figure that scales directly with portfolio size.

That cost doesn't include the additional marketing spend needed to replace each missed lead. Marketing is already the second-fastest-growing operating expense in multifamily housing, up 12.3% year-over-year.* It also doesn't account for staff time spent managing conditional approvals that never convert. The total cost compounds with every vacancy cycle.

*https://www.rentcafe.com/average-rent-market-trends/us/ https://www.rentcafe.com/blog/rental-market/market-snapshots/most-competitive-rental-markets-this-year/ https://www.realpage.com/analytics/retention-climbs-october-2024/ https://www.zumper.com/blog/how-long-does-it-take-to-get-approved-for-an-apartment/ https://www.yardimatrix.com/blog/multifamily-expenses-increase-above-trend-levels /https://www.yardimatrix.com/blog/multifamily-expenses-increase-above-trend-levels/

Incorporating Cash Flow into Your Screening Process

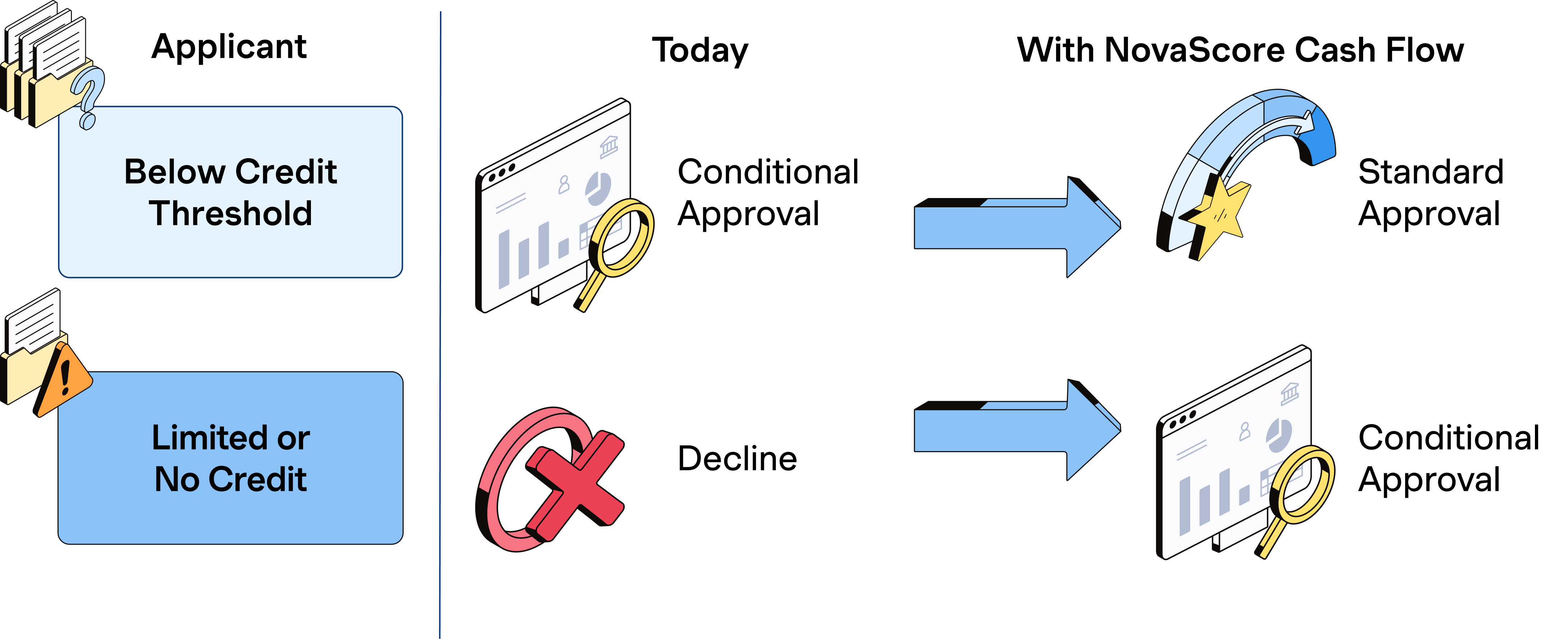

Cash flow screening fills the gap for applicants your credit threshold cannot fully evaluate, without changing anything for those who clear it. In practice, an applicant who falls below your threshold is prompted to securely connect their bank account as part of the application.

Nova Credit's Cash Atlas™ then analyzes up to 24 months of transaction data across three dimensions: income patterns, reserve levels, and spending behavior. Together, those dimensions build a picture of how an applicant actually manages money month to month. That analysis produces a single, actionable cash flow score which equates to a renter’s ability to pay rent on time each month. A cash flow score of 650 or above moves a conditional approval to a standard approval, and converts a decline into a conditional approval with a basis to support it.

Across a portfolio, that translates to higher occupancy, shorter vacancy cycles, and a leasing process that captures qualified renters your current screening would leave behind.

Conclusion

For the renter population which skews heavily toward lower credit scores, a credit-based screening process will decline or conditionally approve the majority of your applicant pool. Some of those applicants are genuinely high risk. Others, whether they have a thin credit file or a low credit score, have the cash balance, income stability, and spending discipline to pay rent reliably every month. A credit score alone cannot tell them apart, but cash flow data can.

As cash flow screening becomes more common, properties using it will consistently capture the best applicants from the declined and conditionally-approved pool. Those who don't adopt it will watch those same applicants land on a competitor's rent roll. Nova Credit makes it easy to get started, integrating cash flow analytics directly into your existing screening process.

To learn more about Nova Credit's cash flow analytics, visit novacredit.com or reach out to connect@novacredit.com.

About Nova Credit

Nova Credit is a credit infrastructure and analytics company that enables businesses to grow responsibly by harnessing alternative credit data, operating as a Consumer Reporting Agency to transform fragmented consumer financial data into compliant, actionable risk insights. Its Cash Atlas™ product gives property managers a predictive cash flow score alongside traditional credit data, surfacing a fuller picture of applicant financial health within their existing screening workflow.